The AIA Pro Achiever has been discontinued. It’s latest version is the AIA Pro Achiever 2.0.

AIA Pro Achiever is an investment-linked insurance plan (ILP). It is a brilliant way to accumulate your wealth and gives you a head start from the word go.

You get open access to a simplified and diversified portfolio from the start.

Here’s our review.

My Review of the AIA Pro Achiever

Now, you may be excited by the potential returns that the AIA Pro Achiever is offering.

But do take note that our calculations later on are purely for illustration purposes only, and the actual performance depends on the funds your financial advisor picks for you.

I like that there are 0% policy fees after the premium payment term, meaning that I can compound my investments with the policy at the fund management charge (up to 1.75%).

Premiums paid after the MIP are also allocated at 105%, a 5% extra every time you commit past the minimum period.

However, my reservations are with the long minimum investment period (MIP).

From the surrender charges, we presume that the MIP is 12 years, as from the 13th year onwards, no charges are incurred should you surrender your policy.

12 years of commitment to an ILP is an awfully long minimum time to get locked into a policy – longer than an economic cycle!

Should you require these funds during your first 12 years, expect to pay hefty surrender charges which will result in a loss for you.

Yes, other ILPs in the market have similar or longer lock-in periods. But these are options for you to choose from – something the AIA Pro Achiever doesn’t offer.

Most ILPs have low MIPs, allowing you to compound your investments to enjoy liquidity and benefit from growth.

The AIA Pro Achiever conversely gets you in for at least 12 years.

Sure, this is not a problem if you have planned your finances properly and have enough cash on hand to withstand tough times.

But if you’re uncertain, you’re better off with ILPs like the Manulife InvestReady III with a low MIP of 3 years and 2.5% fees.

Their fees are also the lowest at 0.7% after the first 10 years, which means that you can let your investment compound and grow faster!

We’ve also compared and ranked the best ILPs in Singapore based on multiple criteria.

However, these are just my preference. Don’t take my preferences as financial advice.

Before making any investment decisions, we recommend seeking a second opinion from an unbiased financial advisor.

This is because you’re about to make a long financial commitment, and you must take some time to understand your alternatives.

If you need help understanding if the AIA Pro Achiever is for you or if there are better options out there, we partner with MAS-licensed financial advisors who are happy to assist.

Criteria

- You need to be between 0-70 years old for the ILP to be issued to you

- Minimum investment amount is S$200 monthly

General Features

The features of the AIA Pro Achiever are as follows:

Premium Payment Terms & Options

The table here shows the minimum regular premiums for each premium payment frequency.

| Premium Payment Frequency | Minimum Premium Amount |

| Yearly | S$2,400 |

| Half-yearly | S$1,200 |

| Quarterly | S$600 |

| Monthly | S$200 |

AIA has the right to make changes to the minimum amounts at any point in time.

Premium Allocation

The table below shows the premium allocations rates for conversion into fund units if you choose to invest with AIA Pro Achiever.

Fund units are purchased with your premium payments at their bid prices on that particular date. Bid price here refers to the highest price a buyer is willing to spend to purchase a unit of a particular fund.

Plan Flexibility

Optional Rider Add-ons

There are 2 riders you can take up with this ILP, namely the Critical Protector Waiver of Premium and Payor Benefit. These riders will obviously require additional charges to add on.

With the Critical Protector Waiver of Premium, should you become gravely sick, your future premiums no longer have to be paid so you can concentrate on recovering.

As for the Payer Benefit, in the event that you pass away, become gravely ill, or disabled, all of your future premium payments will be taken care of by AIA.

This is so that your child or children do not have to worry about needing to take on your future premiums.

Vary Regular Premium

Under AIA Pro Achiever, you will be able to decrease your regular premium amounts but not increase them.

Your premium amounts can be reduced after the 13th annual, 25th semi-annual, 49th quarterly, or 145th monthly payment.

Top-up Premium

Eligibility for top-up premium depends on your track record of paying the premium amounts regularly. Consistent payments of your regular premiums before or on their due dates allows you to make top-ups on an ad-hoc basis.

The minimum amount for premium top-up is S$1,000.

Nevertheless, take note that only 95% of the premium top-ups will be used to purchase your selected fund units as there are charges involved. (Find out more in Fees involved)

Fund units will likewise be bought with your additional top-up at bid prices.

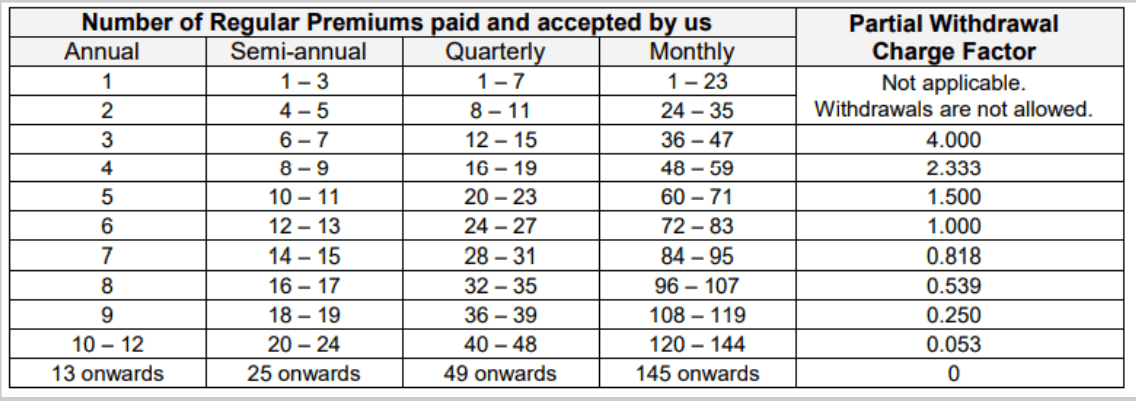

Partial Withdrawal

You have the possibility of making partial withdrawals from your policy after the 3rd annual, 6th semi-annual, 12th quarterly, or 36th monthly regular premium.

The minimum amount allowed for withdrawal is S$1,000, and the total policy value after the withdrawal has to be S$10,000.

However, these amounts can be revised by AIA at any time.

Furthermore, there may be charges associated with your partial withdrawal depending on how far along you are with your premium payments. (See more in Fees involved)

Fund Switching & Automatic Fund Switching

Instruction for switching funds from a particular ILP fund to another can be requested manually or automatically, depending on your choice. There are no charges for fund switching.

The minimum amount required for switching funds is S$50. However, an exception to this rule would be when switching out all fund units from the S$ AIA Money Market Fund.

In this case, the minimum amount required is not applicable.

For automatic fund switching, the switch can occur in fixed intervals, such as monthly or quarterly.

Furthermore, the initial amount in the AIA S$ Money Market Fund has to be S$1,000 before your automatic fund switch.

Automatic Fund Rebalancing

Automatic fund rebalancing refers to units of your invested funds being sold or bought on a regular basis so that your premium allocation follows your pre-specified instructions accordingly.

Under AIA Pro achiever, this flexible option comes for free.

The rebalancing of funds will occur instantaneously after your request to do so is received and accepted.

Your rebalancing instructions will not be acted upon if the fund amount to be rebalanced in or out is less than S$50 or 1% of the policy value.

Premium Holiday

You can take up a premium holiday with no charge under AIA Pro Achiever after paying your regular premium consistently for 13 policy years.

However, should you miss a premium payment before then, your policy will be considered to be on a premium holiday and charges will be inflicted on your ILP. (Check out Fees involved for more)

Full Surrender

As life insurance policies are long term commitments, there may be instances where you might change your mind and wish to surrender your plans early.

As an AIA Pro Achiever’s policyholder, you will be eligible to surrender your policy at any point in time, subject to a written notice submitted to the company. You can yield the entire surrender value of your ILP, which is tabulated by deducting the surrender charge from your policy account value. More on this later.

Policy Termination

If you don’t surrender your plan, your AIA Pro Achiever plan will be deemed to have reached maturity upon you turning 100 years old.

Protection

Death Benefits

With AIA Pro Achiever, the death of the insured will result in AIA paying out the following.

The higher of:

- The sum of your regular premiums paid, add any premium top-ups, less any withdrawals; or

- Your policy value.

Then, any fees and charges applicable to you are deducted from the above amount.

Accidental Death Benefit

In the event that the insured passes away from an injury within 90 days from the accident date, AIA pays an additional 100% of the regular premium payments sum on top of the above mentioned normal death benefit.

Take note that this is only applicable if it happens within the first 2 policy years.

Maturity Benefit

Upon maturity of your AIA Pro Achiever, you will be paid your policy values less any fees and charges. Afterwhich, this would naturally mean that your plan is terminated.

The policy value depends on the prices of the funds in your ILP on its maturity date and thus not a guaranteed amount.

Key Features

Fund offerings

AIA Pro Achiever’s Top 10 Performing Sub-Funds

The AIA Pro Achiever invests in unit trusts.

| Name of Fund | 5-Year Historical Average (%) | Risk Level |

| AIA Global Technology Fund | 30.04 | Higher |

| AIA Greater China Equity Fund | 16.72 | Higher |

| AIA Emerging Markets Equity Fund | 15.29 | Higher |

| AIA Regional Equity Fund | 14.29 | Higher |

| AIA US Equity Fund | 13.44 | Higher |

| AIA International Health Care Fund | 13.19 | Higher |

| AIA Global Equity Fund | 13.14 | Higher |

| AIA Greater China Balanced Fund | 11.39 | Medium to High |

| AIA Acorns of Asia Fund | 10.92 | Medium to High |

| AIA Emerging Markets Balanced Fund | 10.73 | Medium to High |

From: AIA ILP Fund tools

Accurate as of April 2021.

Fees Involved

If you decide to invest in AIA Pro Achiever, the below table covers the different types of fees and charges involved.

| Premium Charge |

|

| Fees and charges below are taken by cancelling and selling fund units at the bid price. | |

| Supplementary Charge |

|

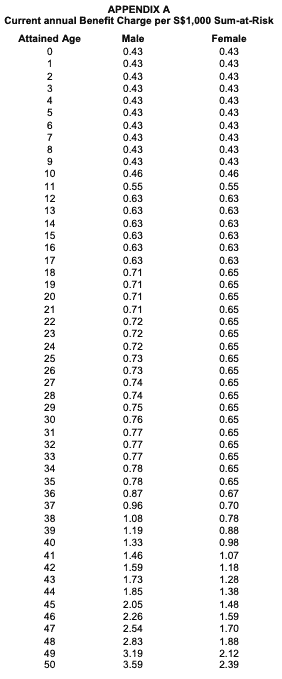

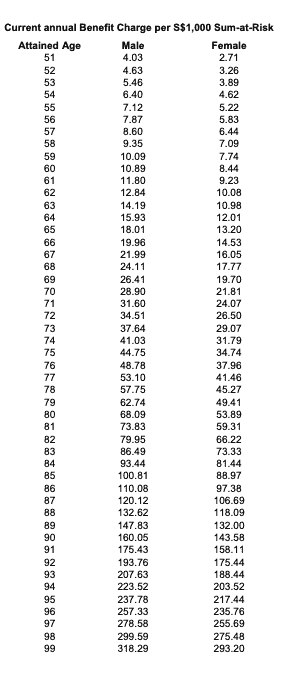

| Benefit charge |

Benefit Charge = (Annual benefit charge rate/12) x Sum-at-risk* *Sum-at-risk = total regular premium amounts paid + total top-ups – total withdrawals – policy value.

|

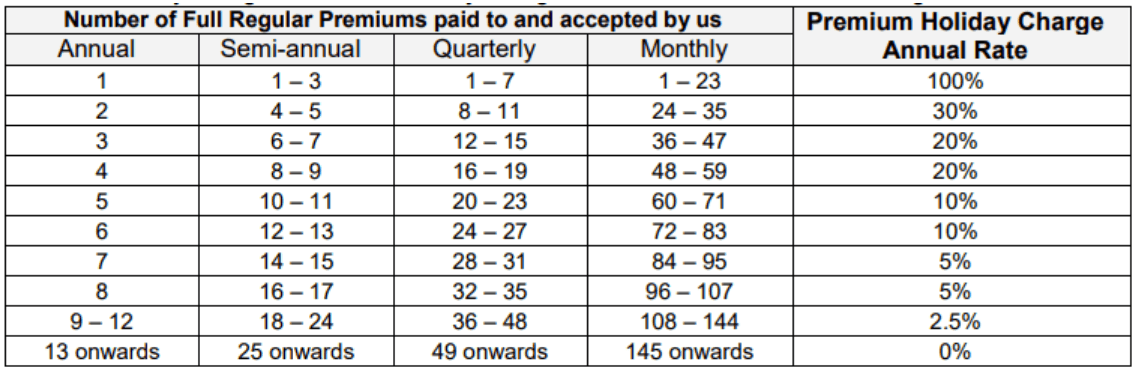

| Premium Holiday Charge |

Premium holiday charge = (Annual premium holiday charge rate/12) x Regular premiums paid

|

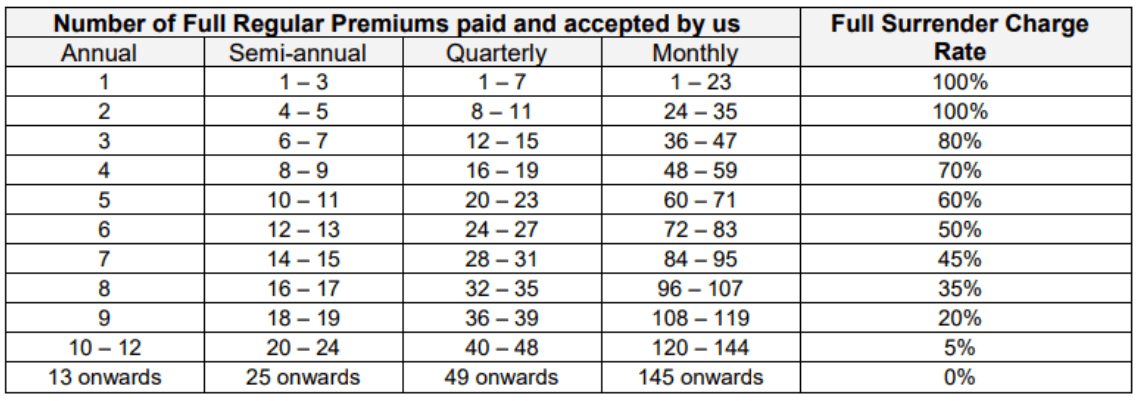

| Full Surrender Charge |

Full surrender charge = Full surrender charge rate x Regular premium policy value.*

*Regular premium policy value refers to the policy value from all the regular premium payments you have made. |

| Partial Withdrawal Charge |

Partial withdrawal charge = Partial withdrawal charge factor x regular premium policy value withdrawn

|

| Fund Management Charge |

|

Compulsory fees

Naturally, you will not need to incur all the abovementioned fees and charges under AIA Pro Achiever. If you were to commit to the policy from start to maturity without any changes, these are the compulsory fees you will incur:

- Supplementary Charge – 2.5% p.a.

- Fund Management Charge – Currently up to 1.75% depending on the funds chosen

Do take note that the supplementary charge is only applicable to you in the first 12 policy years.

How much will I receive upon maturity of the AIA Pro Achiever?

We engaged an AIA advisor, to do the calculation for you.

Assuming that you invest $200 monthly for 12 years and let it compound until the 30th policy year, the funds perform at 10% per annum, you made no withdrawals nor top-ups, and you did not take up any premium holidays; you can expect the below:

First 12 Years | |

| Monthly premium: | $200 |

| Premium Payment Term: | 12 years (144 months) |

| Annual Fund Performance: | 10% |

| Fees in the first 12 years: | 2.5% + 1.75% |

| Net Fund Performance for the first 12 years: | 5.75% |

| Investment value: | $40,292.99 |

Next 18 Years | |

| Fees in the next 18 years: | 1.75% |

| Net Fund Performance in the next 18 years: | 8.25% |

| Total Investment Value over 30 years: | $167,854.04 |

Total Premiums paid: $28,800

Total Interest Earned: $139,054.04

ROI: 482.83%

Take note that because the ILP is investing in AIA’s own portfolio funds, the returns you see are usually not net of fees. Thus, the annual fund management fee will be included.

As our assumed performance rate of 10% is considered as high, this means that the fund we have selected is likely a growth fund.

We used 1.75% for the fund management fee as this percentage is the highest fee rate found out of all the funds offered under the AIA Pro Achiever.

We explain further here in our ILP sub-funds guide.