AIA Secure Flexi Term is a regular premium non-participating term life insurance policy that offers protection at relatively affordable rates and allows you to renew your policy on a regular basis.

It offers additional benefits to enhance your coverage such as the Total and Permanent Disability (TPD) Benefit and the Critical Illness (CI) Benefit.

Here’s our review.

My Review of the AIA Secure Flexi Term

One of the biggest factors when considering a term life plan is its affordability due to the fact that it is the cheapest type of life insurance.

Here, the table shows the premium you would have to pay assuming that you are a non-smoking, 30-year-old male who opts to be insured for $500K.

| China Taiping i-Protect | Singlife Elite Term | AIA Secure Flexi Term | Tokio Marine Term Assure (II) | Manulife ManuProtect Term(II) | PRUActive Term | NTUC Term Life Solitaire | |

| Annual Premium (SGD$) | 498 | 535 | 536 | 545 | 637 | 685 | 733 |

| Total Premium (SGD$) | 19,920 | 21,400 | 21,440 | 21,800 | 25,480 | 27,400 | 29,320 |

*The premium amounts stated in the above table is under the assumption that your policy and premium term under each plan is 40 years (Except AIA Secure Flexi Term: 35 years).

Out of all the policies available, the AIA Secure Flexi Term does not offer a 40-year term plan (till 70) based on our demographic illustration.

As mentioned, its term plan allows for a renewable term of 5, 10, 20, and 30 years and a level term of up to 65 or 75. Thus, we’ve selected a level to 65 years old.

As you can see from the table above, the AIA Secure Flexi Term is one of the cheapest and value for money term life policies.

You can even get a first-year premium discount and subsequent premium discounts of up to 15%, as long as you get healthier and level up your status in your integrated AIA Vitality wellness program.

This would further help to make your policy cheaper and even more affordable.

However, take this with a pinch of salt because it’s only a 35-year plan as compared to 40 years for the rest. We took the yearly premiums and multiplied by 40 years to get $21,440.

Should the premiums be calculated based on a 40-year policy, expect the yearly premium to increase since there’s 5 additional years at ages of higher risk (the older you are, the higher risk it is for AIA).

However, how much increase it’ll be, we can’t say for sure.

Despite the higher premium prices, if you have a family history of cancer or would like coverage for end-stage cancer, you can look into purchasing the AIA Secure Flexi Term as it is the first plan in the market to provide a terminal cancer benefit.

You can also think about getting this plan for your kids as they can be covered up to $500,000.

Like most other plans, this policy is also renewable and convertible.

Despite it’s advantages, if you compare it against other term plans in Singapore, the AIA Secure Flexi Term does lose out quite a bit.

For instance, if you’re looking to counter the effects of inflation or looking for a term to 99 plan, the HSBC Life Term Protector is better.

Looking for the cheapest? The China Taiping i-Protect takes the cake here.

If you wanna talk about flexibility and coverage for ECI or ECI, then the Singlife Elite Term is the most popular plan for these scenarios.

With so many nuances in individual scenarios and goals to consider, it’s difficult to find what’s the best for you.

I suggest starting your research by reading our post on the best term life insurance plans in Singapore so that you understand what are your possible alternatives.

After doing that, you might want to consider engaging an unbiased financial advisor for a second opinion to whether the AIA Secure Flexi Term is the best for your needs.

Given that term life insurance plans are 20 to 30 years worth (sometimes more) of commitment, it’s best you take your time to explore other options so that you don’t make financial decisions you’ll regret in the future.

And based on our experience running Dollar Bureau, this happens more often than you think.

If you need someone to assist you with finding the best term plan for yourself, we partner with MAS-licensed financial advisor that are more than happy to help!

Click here for a non-obligatory chat.

Now let’s dive deep into what the AIA Secure Flexi Term offers.

General Features

Policy Terms

AIA Secure Flexi Term allows you to select between 2 options for your coverage term. You have the choice of choosing a renewable term of 5, 10, 20, or 30 years, or a level term of up to 65 or 75 years old.

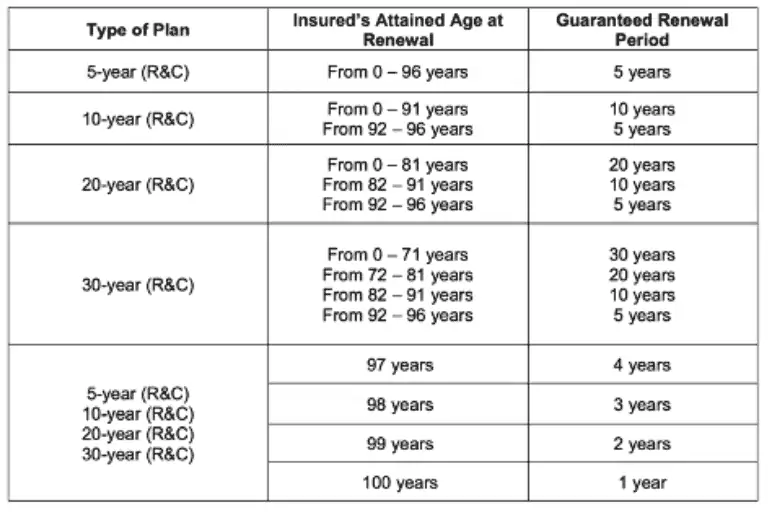

You can renew your policy at the end of each term until the age of 101.

Premium Payment Terms & Options

Your premiums are due for the duration of your basic policy, and the rates are guaranteed and will stay constant during the policy term you select.

Do note that at the policy renewal time, the premium rates are based on the rates applicable to the life assured’s age and are not guaranteed at that time.

These prices may be modified depending on future experience or to satisfy AIA’s responsibilities under the basic policy and/or Singapore laws and regulations as they change.

You can also choose to combine your AIA Secure Flexi Term policy with AIA Vitality which provides you with a premium discount as well as future Vitality Status-dependent premium discounts. With this, you will receive bigger savings of up to 15%, which equals cheaper coverage costs.

Protection

Death Benefit

AIA shall pay the Death Benefit, which is the Insured Amount less any monies owed to AIA, if the Insured passes away while the basic policy is in effect.

According to the policy, AIA’s responsibility is restricted to a refund of the whole premiums paid, without interest, if the life guaranteed commits suicide within one year of the basic policy’s issuance date or reinstatement date, whichever is later.

This always applies unless otherwise specified in any supplementary agreements or endorsements.

Terminal Illness Benefit

AIA will pay the Terminal Illness Benefit, which is the Insured Amount less any monies owed to AIA, if the life assured is diagnosed with Terminal Illness while the policy is in effect.

According to AIA, the term “Terminal Illness” refers to a confirmed diagnosis of an illness that is likely to cause the life assured’s death within 12 months.

This benefit accelerates payment of the basic policy’s insured amount.

This benefit is subject to the Terminal Illness per life limit of $20 million, in addition to the other underwriting limitations applicable to this plan (aggregated with other policies or supplementary benefits issued on the same life).

For insurance issued in other currencies, a conversion rate established by the firm will be used.

Terminal Cancer Benefit

AIA will pay the Terminal Cancer Benefit, which is the Insured Amount less any monies owed to AIA, if the life assured is diagnosed with a Terminal Cancer while the policy is in effect.

According to AIA, the term “terminal cancer” refers to a malignant tumour that has been verified by histology and is at a stage in which all of the following characteristics are present:

- Cancer falls under end-stage cancer, which is defined as cancer that has spread to at least one distant organ. Cancer in its last stages also includes Chronic Lymphocytic Leukemia stage 4 (RAI classification) and lymphoma stage 4. (LUGANO classification).

- Cancer treatment cannot stop the spread of the disease. The use of surgery, radiation, medicines, and other therapies to cure, shrink, or stop the progression of cancer is referred to as cancer treatment.

- The doctor can only provide palliative care to the patient.

This benefit accelerates the payment of the basic policy’s insured amount.

This benefit is subject to the Terminal Cancer per life limit of $1 million (or $500k for juvenile) in addition to other underwriting limitations applicable to this plan (aggregated with other policies or supplementary benefits issued on the same life).

For policies issued in other currencies, the company’s conversion rate will be used.

Note that an insured will be deemed a juvenile until he/she:

- reaches the age of 16 and is working or self-employed; or

- reaches the age of 21,

whichever comes first.

Additional Features & Benefits

Automatic Renewal

Your policy will be automatically renewed without further underwriting if the following conditions are met:

- the policy is in effect the day before the date of renewal;

- there are no premiums due the day before the renewal date; and

- AIA receives and accepts payment for policy premiums based on the Insured’s age at the time of renewal.

Please refer to the Renewal Privilege Guide Table below for each type of plan.

Conversion Policy

AIA permits you to change your basic policy to a whole life, endowment, or investment-linked policy that provides equal or similar cover (as determined by AIA), which is available for conversion at any time without further medical underwriting up to the current Insured Amount, provided that:

- the basic policy is in place on the date of your conversion request and will remain in effect until the day before the conversion takes effect;

- there is no late premium for the policy as of the date of your conversion request and up to the day before the conversion takes effect;

- on your policy, no claim has been reported for the insured;

- on or before a policy anniversary of the basic policy prior to the Insured’s 70th birthday, your request for conversion is submitted, and any resultant conversion takes effect;

- AIA receives and approves the new policy application; and

- AIA receives and accepts payment for the new policy’s premiums, which will be calculated based on the rates in force and the insured’s age at the time of conversion.

Add-on Riders

AIA Secure Flexi Term offers additional benefits to provide extra support.

Total and Permanent Disability (TPD) Benefit

This is an expedited benefit that accelerates the basic policy’s death benefit. Note that when the death benefit is fully accelerated, the policy will immediately end.

TPD implies that the Insured is unable to undertake or carry out any employment, occupation, or profession in order to earn or acquire any earnings, compensation, or profit prior to the policy anniversary occurring on or immediately after the Insured’s 65th birthday. The coverage is up to age 65, and slightly after your 65th birthday.

Such impairment must last for at least 6 months and there is no chance of recovery for an extended period of time. This case does not apply to juveniles.

TPD means the Insured is unable to perform at least 2 of the following 6 Activities of Daily Living (ADLs), even with the help of special equipment. It also implies that the insured constantly requires the physical help of another person throughout the whole activity.

The following are considered as ADLs:

- Washing

- Dressing

- Feeding

- Toileting

- Mobility

- Transferring

Any of the following circumstances will be instantly recognised as TPD (applied to juveniles as well):

- complete and irreversible loss of vision in both eyes; or

- loss via entire amputation or total and irreversible loss of function of 2 limbs at or above the wrist or ankle; or

- complete and irreversible loss of vision in 1 eye; and

- loss due to total amputation of 1 limb at or above the wrist or ankle; or

- total and irreversible loss of function of 1 limb above the wrist or above the ankle.

AIA will only accept these circumstances as TPD if the insured is a minor.

This benefit is subject to the TPD per life maximum of $7.5 million in addition to any underwriting restrictions applicable to this plan (aggregated with other policies or riders issued on the same life). For policies issued in other currencies, the company’s conversion rate will be used.

Note that the duration of this additional benefit will be the shorter of:

- the policy term; or

- the number of years from the issue date of this benefit to the policy anniversary that occurs on or right after the Insured’s 70th birthday.

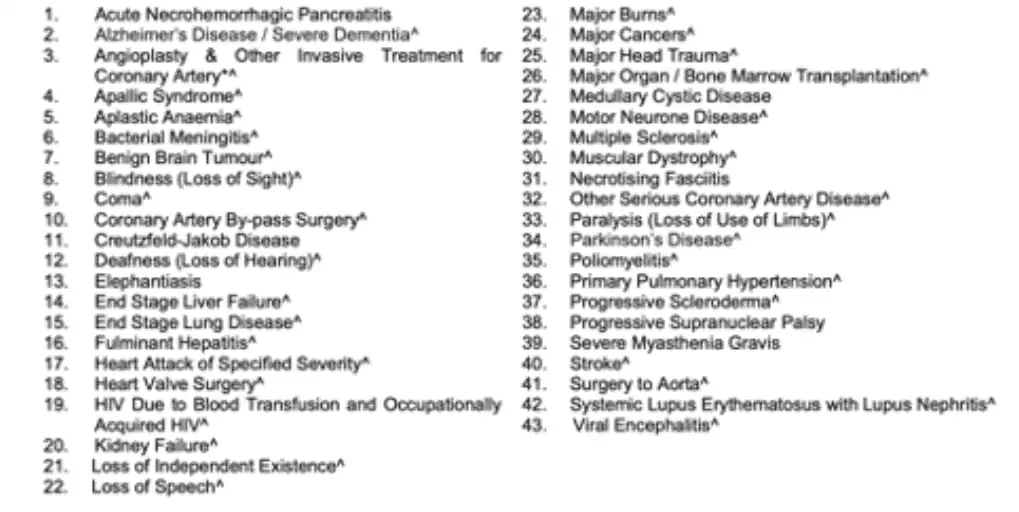

Critical Illness (CI) Benefit

AIA will pay the Insured Amount of this additional benefit if the Insured is diagnosed with any of the listed Critical Illnesses.

The Insured Amount of your basic policy will be decreased in proportion to the Insured Amount of this additional benefit. Any further benefits payable under the policy, as well as any future premiums, will be calculated using the reduced Insured Amount.

This benefit covers the following CIs:

This benefit will be available for the same length of time as the basic policy.

For this additional benefit, AIA will pay up to $25,000 if the insured undergoes Angioplasty & Other Invasive Treatment for Coronary Artery.

This additional benefit will only be payable once during the additional benefit’s period and will terminate immediately upon payment.

However, there are a few circumstances in which no benefits will be paid. This benefit does not cover CIs caused directly or indirectly, in whole or in part, by any of the following events:

- illnesses or surgical procedures other than a diagnosis of a disease or the conduct of a surgical operation under a Critical Illness;

- diseases, impairments, pre-existing illnesses, or conditions that the insured is suffering from before the issue date or reinstatement date of this benefit, whichever comes later, unless a declaration was made in the application and was accepted by AIA;

- when the diagnosis of Fulminant Hepatitis or Major Cancers of the Insured was, in AIA’s judgment, caused by an Acquired Immunodeficiency Syndrome (AIDS) or infection with any Human Immunodeficiency Virus (HIV); or

- Severe Acute Respiratory Syndrome (SARS). SARS complications, on the other hand, maybe acceptable with a diagnosis of End-Stage Lung Disease if the contract definition, diagnostic criteria, and specific proof specified under End-Stage Lung Disease are met.

Please remember that the premiums for this benefit are not guaranteed. The premium rates may be adjusted in the future depending on future experience and any modifications or amendments to Singapore’s laws and regulations.

AIA will not pay any benefits for Heart Attacks, Major Cancers, By-pass Surgery, Angioplasty & Other Invasive Treatment for Coronary Artery, or Other Serious Coronary Artery Diseases if the date of diagnosis of any conditions leading to the performance of these surgeries or treatments to the Insured occurred within 90 days of the later of:

- the date of issue of your policy or this benefit, whichever comes later; or

- the date of reinstatement of your policy of this benefit, whichever comes later.

References

https://www.aia.com.sg/en/our-products/life-protection/aia-secure-flexi-term.html