The Aviva MyWholeLifePlan (IV) has been renamed to the Singlife Whole Life as of 16 August 2022.

The Singlife Whole Life is a whole life insurance policy that provides basic protection for death and terminal illnesses.

It also allows for customisation and flexibility of multiplying up to the five times the sum assured, enhancement of total and permanent disability coverage and critical illness coverage, as well as with the option of several other optional riders.

As a participating policy, it accumulates cash value in the form of guaranteed and non-guaranteed bonuses.

My Review of the Singlife Whole Life Plan

The Singlife Whole Life policy offers a comprehensive blend of flexibility, protection, and potential for wealth accumulation, catering to individuals seeking long-term financial security and benefits that extend beyond mere savings.

Here are some pros & cons of the Singlife Whole Life plan:

Pros

- Flexible Premium Payment Terms: The Singlife Whole Life plan provides a range of premium payment terms, including single premium or regular premium options with terms of 10, 15, 20, and 25 years, or up to the age of 65. This flexibility allows you to choose a payment schedule that aligns with your financial capacity and goals, making it easier to manage your long-term financial planning without overburdening your current financial situation.

- Comprehensive Protection: Singlife Whole Life offers a robust death benefit, ensuring that your beneficiaries receive a lump sum upon the your demise. Additionally, the policy includes terminal illness benefits and provides financial support when it’s most needed. Adding up to 400% additional coverage for basic and selected supplementary benefits further enhances the policy’s value as a protective measure for you and your family.

- Additional Cover and Benefits: The policy’s structure allows for an increase in coverage during significant life events without the need for medical underwriting, ensuring that policyholders can adapt their coverage to changing life circumstances. This feature is particularly valuable for those who experience major life milestones and wish to ensure adequate insurance coverage.

- Wealth Accumulation and Flexibility: With the option for income payout starting from age 65, you can supplement your retirement income, providing a steady stream of funds to support your lifestyle in retirement. The policy’s participation in the insurer’s fund allows for potential reversionary and terminal bonuses, offering an opportunity for wealth growth over the policy’s term.

Cons

To be honest, the Singlife Whole Life plan is a pretty well-balanced plan and is competitively priced, so there’s not much cons that come with the policy.

However, I do have to point out a con:

- High Expense Ratio: While Singlife’s participating fund has shown decent growth, the high expense ratio compared to the industry average could impact your final profits and bonuses. This factor is crucial for those looking for a long-term policy that could maximise their savings.

While I don’t think that high expense ratios are an issue if the participating fund can produce higher annualised returns, this is not the case with Singlife’s par funds.

If you were to take a look at the following table, you’ll realise that Singlife’s high expense ratios do not translate to better results, as compared with Manulife’s high expense ratios, but has the highest long-term returns.

But it’s not all that bad as Singlife’s par funds are ranked 4th amongst 8 positions, and it is possibly a worth trade-off for more flexibility and customisations from a whole life insurance plan.

We also found that Singlife’s guaranteed returns were the highest when we compared all whole life policies in Singapore – so if you’re leaning more towards the safer side, then the Singlife Whole Life might suit you better.

In summary, the Singlife Whole Life plan is well-suited for individuals seeking a flexible and comprehensive insurance solution that offers both protection and potential for wealth accumulation.

However, it’s essential to consider the policy’s complexity, cost, and long-term commitment, alongside the insurer’s fund performance and expense ratio, to ensure it aligns with your financial goals and circumstances.

As usual, we recommend that you get a second opinion on whether the Singlife Whole Life is the best whole life insurance plan for you.

As you’ll rely on this policy for death, TPD, TI, possibly ECI/CI, and the cash value upon retirement, it’s best that you take extra time to make sure that the Singlife Whole Life is truly the best for you.

If you’d like to get a second opinion, we partner with unbiased financial advisors who represent multiple insurers and are able to compare policies for you.

This way, you’d get impartial advice and find a suitable policy.

Click here for a free second opinion.

Here’s more about the Singlife Whole Life plan:

Criteria

- Minimum sum assured of S$50k.

Basic Product Features

Premium Payment Terms

The Singlife Whole Life is both a single premium or regular premium policy with flexible payment term options – 10,15, 20, and 25 years, or up to the age of 65 years old.

Your final premium amount is determined by factors such as age, gender, smokers status, sum assured, policy type, and length of premium period.

Protection

Death Benefit

A lump sum is paid upon the death of the insured.

Additional Cover and Additional Cover Period

- Additional Protection Coverage applicable within the duration of the Additional Cover Period for the Basic Benefits such as the Death Benefit and Terminal Illness Benefit, and selected Supplementary Benefits such as Total and Permanent Disability Advance Cover IV, Critical Illness Advance Cover V, and Early Critical Illness Advance Cover V.

- You can opt for the Additional Protection Coverage to be either 100%, 200%, 300%, or 400% of the basic plan’s assured sum, or of the applicable supplementary benefits.

- The Additional Cover Period is valid from the policy effective date up till the policy anniversary when your chosen Additional Cover attains its maturity date.

The Additional Coverage amount and duration will be selected during policy application with no amendments allowed thereafter, and will automatically be terminated if the policy is converted to Reduced Paid Up (RPU) Insurance or Extended Term Insurance (ETI).

After the Additional Coverage ends due to the above-mentioned reasons, the policy continues to be active based on the:

- RPU sum determined by Singlife or

- Prevailing Base Sum Assured for a coverage period as determined by Singlife in the case of ETI.

Terminal Illness (TI) Benefit

Upon the diagnosis of Terminal Illness, Singlife will payout a lump sum as an advancement of the Death Benefit.

To qualify for the TI Benefit, the insured is required to be diagnosed with an illness that results in death within 12 months.

The policy will automatically be terminated once the Terminal Illness benefit has been paid out.

Other Features and Benefits

Surrender Benefit

Upon the third policy year, your policy will acquire cash value as long as premiums are paid in a timely manner.

If you have opted for the income payment option, the cash surrender value will be adjusted for the monthly income paid out.

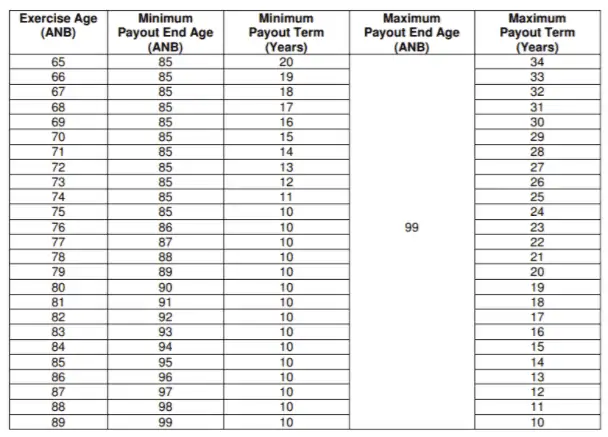

Income Payout Option

From the age of 65, you may opt to supplement your retirement needs and lifestyle, you may decide to exercise the Income Payout Option which provides you with monthly income.

The policy continues to provide you with coverage after the Income Payout Option is exercised. The sum assured will be adjusted based on the monthly income paid out and the cash surrender value of the surrender benefit. You will also continue to be entitled to the Reversionary Bonus for the base sum assured and the Terminal Bonus.

Upon the death of the insured, there are benefits available for payout if the Income Payout Option is opted for.

Waiver of Interest Benefit

If you are between the age of 19 to 75, and face the inability to make premium payments due to involuntary retrenchment or unemployment for a period of at least 3 consecutive months, you have the option to exercise the waiver of Interest Benefit.

This is provided you submit satisfactory evidence within 6 months of retrenchment or unemployment.

Upon approval of the benefit, you are exempted from the payment of the automatic premium loan’s interest amount on any instalment premiums from the date when you are retrenched or unemployed, up till a maximum of 12 months or when you are in permanent and gainful employment, whichever is earlier.

The overdue premium accumulated has to be paid in full within the next 12 months from the end of the Waiver of Interest Period.

There will be interest incurred if the overdue premiums are not paid in full within this Repayment Period.

The Waiver of Interest Benefit can be exercised up to 2 times per policy.

Guaranteed Extra Protection Option

Purchase a new non-participating level term Supplementary Benefit, without any health proof, when you are at any of the following significant life stage event(s):

- Legal marriage, divorce, or widowed.

- Birth of a newborn baby or legal child adoption.

- Purchase of a property.

- Your child enrols into tertiary education.

- When you enter full-time employment within one year of tertiary education graduation.

The non-participating level term Supplementary Benefit provides coverage for death and TI. You can choose to exercise this benefit from the age of 10 years up till the age of 99.

The premium will be calculated based on your age when this Supplementary Benefit is opted for.

This Supplementary Benefit continues to be in force, so long as you continue to make premium payments.

The Guaranteed Extra Protection Option can be exercised up to 2 times, regardless of the number of policies you might have that offer similar benefits.

Policy Loan

You have the option to request a Policy Loan of up to 90% of the cash surrender value less any payables to Singlife, if you have not exercised the Income Payout Option.

There will be a minimum loan amount and policy loan rate which are subject to changes according to Singlife’s terms and conditions. The interest rate is non-guaranteed.

Add On Riders

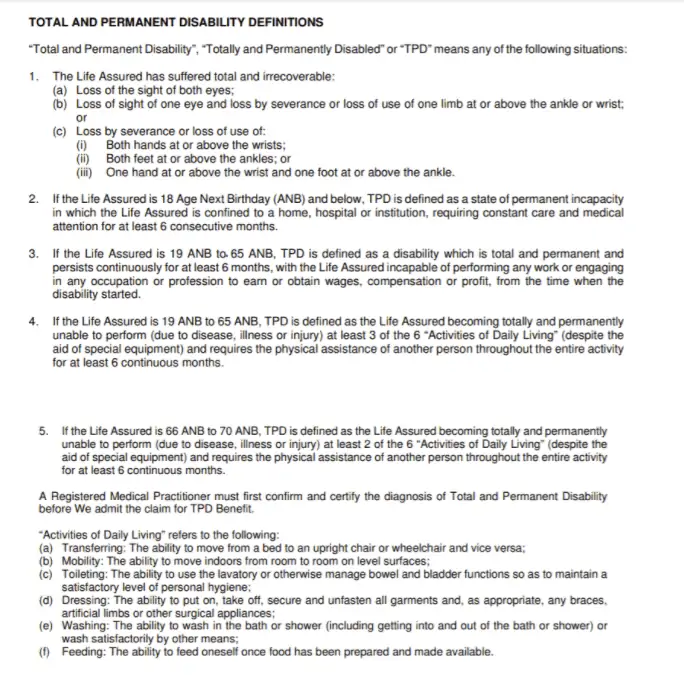

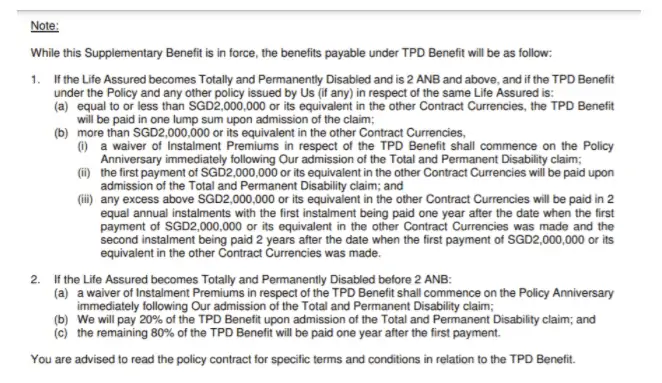

Total and Permanent Disability Advance Cover IV

Provides coverage for disabilities that are total and permanent. The payout under this supplementary benefit is an advancement and reduction of the Death Benefit.

Critical Illness Advance Cover IV

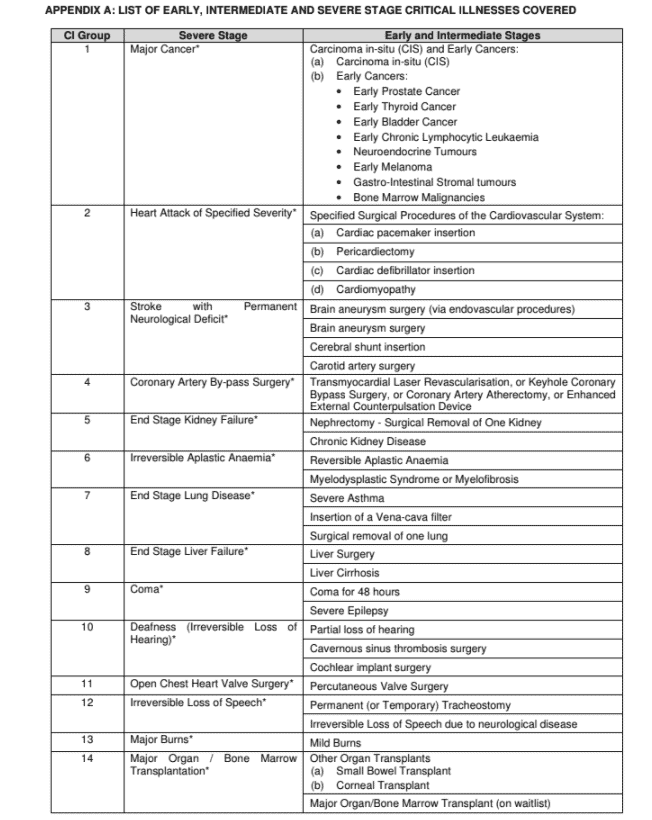

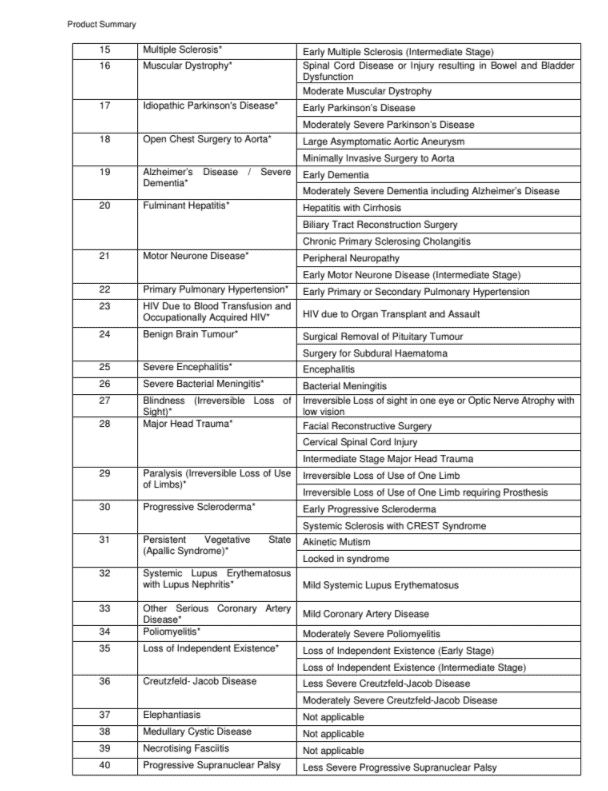

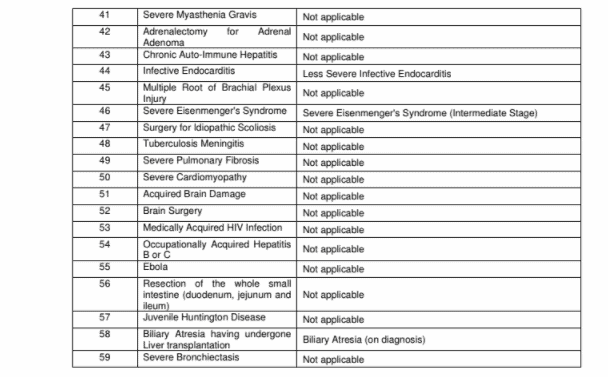

A lump-sum payout as an advancement of the death benefit is done if you are diagnosed with any of the advanced stage critical illnesses covered. More on this later.

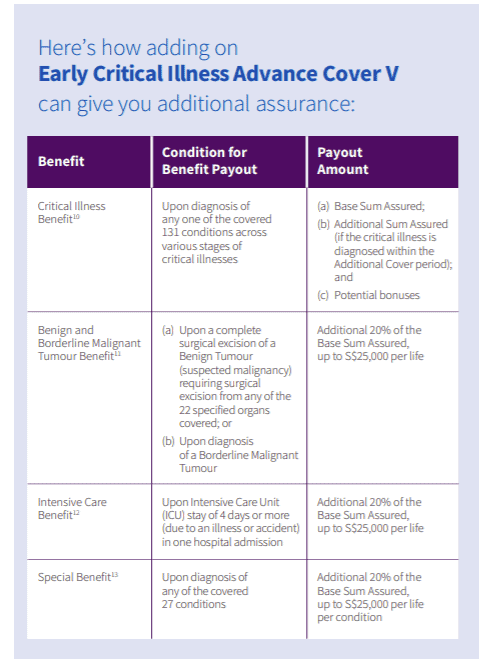

Early Critical Illness Advance Cover V

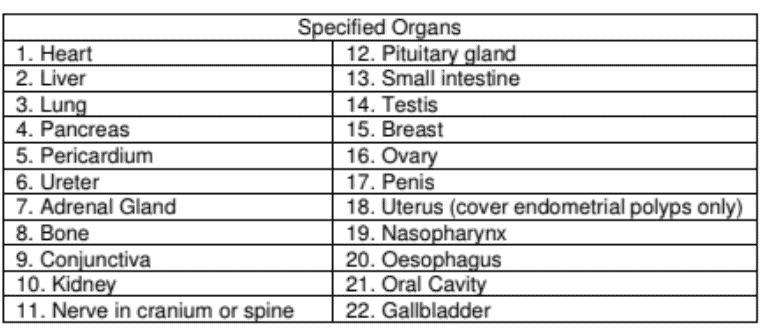

With the Early Critical Illness Advance Cover V, you extend your critical illness coverage to 59 late-stage and 72 intermediate and early-stage CIs.

Benign and Borderline Malignant Tumour Benefit – 22 specified organs covered for Benign Tumour (suspected malignancy) requiring surgical excision.

Critical Illness Premium Waiver II/ Payer Critical Illness Premium Waiver II/ Payer Premium Waiver

Allows waiver of premium payment, if you are diagnosed with a critical illness of any stage or if the payer of the insurance premium is diagnosed with a critical illness, faces death, or total permanent disability.

These are the CIs and ECIs covered by the Singlife Whole Life.

Bonus Features

Reversionary Bonuses

Singlife might allocate a reversionary bonus annually, but the bonus rate is not guaranteed.

Upon declaration, the reversionary bonus becomes guaranteed and will be paid out, regardless of the performance of the participating fund, less any payables to Singlife.

You can withdraw the reversionary bonus in cash value, but your bonus payout will be less than the guaranteed accumulated reversionary bonus. The cash value of the accumulated reversionary bonus will be determined by Singlife.

After withdrawal, your policy continues to be active with zero accumulated reversionary bonus. Future reversionary bonuses can be added to the policy.

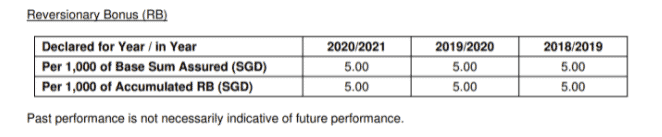

We provide you with the following illustration for a clearer understanding. For example, with a return of 4.25% p.a, the reversionary bonus is S$5.00 per $1,000 sum insured.

The annual compounding rate determines the interest built up on reversionary bonuses.

The below table illustrates the Reversionary Bonus for the past three years.

Terminal Bonus

Upon policy termination due to a claim, surrender or maturity, you might receive an additional bonus if Singlife declares a non-guaranteed terminal bonus, less any payables to them.

The terminal bonus is indicated as a percentage of the accumulated reversionary bonus surrender value and the bonus might vary, depending on when the insured surrenders his or her policy.

With this being a new plan, past indicative results of Terminal Bonus are presently not available.

Participating Fund Performance

The Singlife Whole Life is also a participating policy that allows you to accumulate cash value in the form of guaranteed and non-guaranteed bonuses.

Annual Investment Performance

Singlife’s participating fund in recent years has generally been performing well.

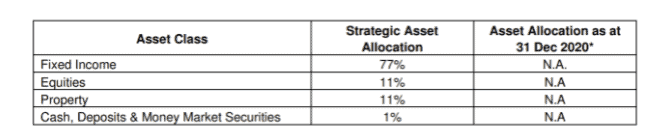

The table below illustrates the investment mix of the Singlife Whole Life based on strategic asset allocation.

Due to it being belonging to a new investment pool within the par-sub-fund, the actual investment mix is currently not available.

The actual asset allocation might slightly differ from the Strategic Asset Allocation indicated above but will fall between the asset allocation range stated.

There is also no historical performance for this policy due to it being a new investment pool within the par-sub-fund.

Geometric Average

The Geometric Average will be more suitable and accurate in calculating profits for investment portfolios such as that of participating funds.

Instead of just taking the average rate of return, the geometric average takes into account compounding and returns and losses, which has a part to play in the amount reinvested in the following years.

Singlife has been one of the few better-performing participating funds based on geometric average net investment returns on participating funds, with steady growth for the past decade and 5 years, leading to being the top 5 performers for the past 3 years (2017-2019), at 6.9%, higher than the group average of 6.69%.

Expense Ratio

Singlife has a pretty high expense ratio against the average expense ratio in the past 3 years. The expense ratio is one of the important factors to take note of as it can significantly affect the final profits generated for the participating fund.

Overall Performance

Singlife has maintained decent growth for its participating funds over the past decade.

But they have a pretty high expense ratio, above the industry average in 2019. This might be a point to consider for those who are looking for insurers with a steady and healthy participating fund record.

The results mentioned above are based on past fund performance and may not indicate future profits and results.

It is also important to understand that the final returns distributed to you are not the same as the funds’ rate of returns. The bonuses are decided and declared by Singlife.