Hedge yourself from unexpected situations life throws at you with a participating endowment plan like PRUFlexi Cash, which provides the flexibility of receiving benefit payouts every year.

My Review of the Prudential PRUFlexi Cash

The PRUFlexi Cash is a popular endowment plan that many individuals seek. Personally, I’m not a big fan of endowment plans due to the long lock-in periods and low actual returns so my review of the PRUFlexi Cash might be pretty skewed.

However, I’ll do my best to be objective.

In my opinion, if you’re someone looking to force yourself to save money in the long-term or foresee a life event at the end of the maturity period, you can consider getting this.

The good thing is that this policy allows you to take a small portion of your savings after the end of your second policy year so that you can enjoy your efforts or for other needs.

Another positive note is that its par funds perform at an impressive 5.77% over the past 10 years (data is outdated, though).

Furthermore, the wide range of riders offered is more than what most competitors are offering. So if you purchased a rider on top of your basic policy, you’ll be able to waive premiums depending on your coverage.

A thing to note is that this policy does not have a breakeven point and that even in the 15th year, you will only receive $144,000 of guaranteed payout as compared to $188,520 premiums paid.

This is a huge dealbreaker for me as I prefer to have my premiums guaranteed and receive the non-guaranteed portion as a bonus.

The Manulife ReadyBuilder has a breakeven point at the 15 policy year and offers similar features at the PRUFlexi Cash – without the Yearly Cash Benefit.

However, this is purely my opinion and based on what I prefer for my own financial planning. What works for me might not work for you.

Perhaps our guide to the best endowment plans might help you decide better.

Once you understand your available alternatives, you can proceed to get a second opinion to whether the Prudential PRUFlexi Cash is the best option for you – especially since it requires a minimum commitment of 15 years.

Should you need an unbiased financial advisor to get a second opinion from, we partner with MAS-licensed financial advisors to assist you with this.

Criteria

- Minimum premium payment period of 15 years

Features

Policy Terms

Choose between a policy term of 15, 20, or 25 years with the PRUFlexi Cash Plan.

Furthermore, you are also able to select the frequency of your premium payments namely, monthly, quarterly, half-yearly, or yearly.

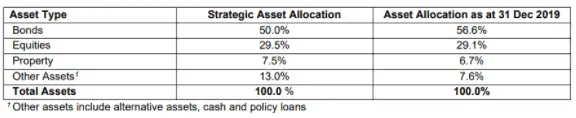

Premium Allocation

Since minimum premium amounts are net, meaning that fees and charges have already been considered and 100% of your premiums paid will be allocated to purchase the participating fund units.

As of 31st December 2019, the allocation of your premiums is as shown in the table below.

Payout Options

Under the PRUFlexi Cash Policy, you have 3 payout options to choose from as follows.

- Yearly Cash Benefit paid out to you starting from the end of your 2nd Policy Year; or

- Deferred Yearly Cash Benefit (larger amounts) paid out to you after the end of your 10th Policy Year*; or

- Reinvest your Yearly Cash Benefit back into your policy to be accrued daily at a non-guaranteed interest rate.

*For this payout option, you can choose to defer the Yearly Cash Benefit payout up to a year before the end of your policy term.

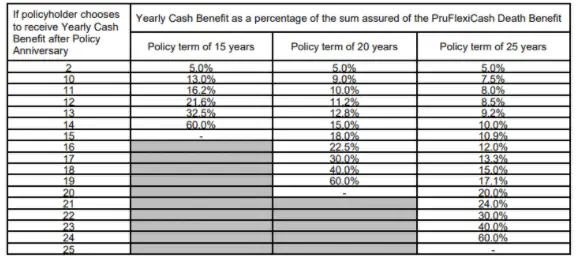

The table below shows the different percentages depending on when you choose to receive your Yearly Cash Benefit.

Maturity Benefits

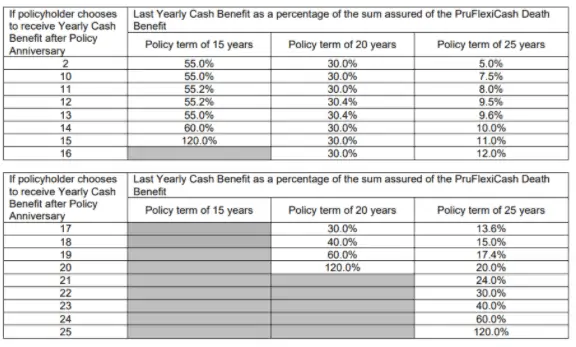

Receive maturity benefits consisting of your last Yearly Cash Benefit plus any bonuses entitled to you in your last policy year.

The table below shows the different percentages you shall receive in your last Yearly Cash Benefit depending on when you have elected to start collecting this annual benefit and your selected policy term.

The Maturity Bonus you shall receive is non-guaranteed and are explained further in the Bonus Features section.

Flexibility

The following table displays the flexible features that you can choose from under your PRUFlexi Cash policy.

| Flexible Feature | Additional Description |

| Partial Surrender of your Reversionary Bonus |

|

| Automatic Premium Loan, Policy Loan and Surgical & Nursing Loan |

|

| Option to buy another Endowment or Term policy without evidence of good health on selected life events |

Selected life events refer to:

|

If the person insured is a child:

|

Bonus features

The bonuses form the non-guaranteed portion of the benefits under your plan. Any illustrations below are under the assumption that PRUFlexi Cash’s participating fund yields a return rate of 4.75% per annum.

Reversionary Bonus

After your policy’s 2nd anniversary, Prudential may announce a Reversionary bonus to you annually.

As long as the company has declared it, this bonus will become a guaranteed benefit for you and be accumulated in your policy.

Here are the reversionary bonus amounts declared in previous years.

| Year | Reversionary Bonus per $1,000 Sum Assured | Reversionary Bonus per $1,000 on accumulated Reversionary Bonus |

| 2015, 2016, 2017, 2018, 2019. | SGD15.00 | SGD35.00 |

Please be aware that past performances do not predict nor guarantee future results.

Performance Bonus

The Performance Bonus is paid out to you once under any of the following situations.

- When you surrender the policy; or

- When you claim on a basic benefit of your policy; or

- When your policy matures.

As illustrated in the table below, the Performance Bonus amount to be paid out is expressed as a percentage of your accumulated Reversionary Bonus which changes according to your policy termination date.

The illustrated Performance Bonus rates as a percentage of the accumulated Reversionary Bonuses are as follows:

| No. of completed years in force | Performance Bonus as a percentage of accumulated Reversionary Bonus (%) |

| 1 | 0.0 |

| 2 | 0.0 |

| 3 | 39.0 |

| 4 | 42.0 |

| 5 | 45.0 |

| 6 | 48.0 |

| 7 | 51.0 |

| 8 | 54.0 |

| 9 | 58.0 |

| 10 | 62.0 |

| 11 | 66.5 |

| 12 | 70.5 |

| 13 | 74.5 |

| 14 | 78.5 |

| 15 | 82.5 |

| 16 | 85.0 |

| 17 | 88.5 |

| 18 | 92.5 |

| 19 | 97.0 |

| 20 | 104.0 |

| 21 | 107.5 |

| 22 | 111.0 |

| 23 | 114.5 |

| 24 | 118.0 |

| 25 | 120.5 |

Maturity Bonus

Likewise, the Maturity Bonus is a one time amount calculated as a percentage of your accumulated Reversionary Bonus, which might be paid out to you upon the maturity of your plan.

The table below displays an illustration of the different Maturity Bonus Rates depending on your chosen policy term.

The illustrated Maturity Bonus rates as a percentage of the accumulated Reversionary Bonuses are as follows:

| Policy Term (Years) | Maturity Bonus as a percentage of Accumulated Reversionary Bonus (%) |

| 15 | 50.0 |

| 20 | 20.0 |

| 25 | 0.0 |

Past rate of return of the investment

The following table shows the net past return rate of the participating fund, whereby the expenses have already been subtracted.

Protection

Death Benefit

Upon the death of the person insured, the full sum assured for death will be paid out. Any accumulated bonuses will also be paid out.

Naturally, any amounts owed to Prudential will first be deducted from your payout sum.

Within one year from policy commencement, the insured will not be eligible for the death benefit if he/she passes away from any pre-existing conditions or suicide.

Accelerated Terminal Illness Benefit

In the event that you suffer from a terminal illness (TI), you will be eligible to receive this Accelerated Terminal Illness Benefit provided that you are covered for it during the cover period.

Prudential defines TI as a sickness that would lead to the person assured to pass away within a year that has been diagnosed by a Registered Medical Practitioner.

Moreover, the Registered Medical Practitioner would have to be certified with a western medicine degree and be licensed by the relevant medical authority in Singapore to practice medicine. This would mean that you cannot head to a Traditional Chinese Medicine(TCM) for your TI diagnosis, no matter how much you believe in him/her.

Accelerated Disability Benefit

The Accelerated Disability Benefit is paid out to the person insured if he or she becomes completely and permanently disabled before the expiry of the coverage.

Naturally, any amounts owed to Prudential will be deducted first.

The table below shows the different Accelerated Disability Benefit amounts to be received at the point of becoming disabled, based on the insured person’s age on their last birthday.

| Age (on last birthday) at date of Disability | Payout Value |

| Below 1 years old |

|

| 1 to 64 years old |

|

When 100% of your assured value and proportionate bonuses that has been added to your policy exceeds S$2,000,000, the remaining amount is paid out at the earliest of:

| |

*Exceptions to the Deferment Period:

| |

Prudential shall stop making payouts at once, should you recover from your full and enduring disability before the end of your payment term.

After which you are still able to continue with the plan and be eligible for Death and TI Benefit, so long as you pay the necessary premiums. Your sum assured will now be equivalent to any amount exceeding the S$2,000,000, which was previously an outstanding payout.

Surrender/Ending the Policy

You may choose to end your policy on your own accord by fully surrendering your plan. If you decide to surrender your plan after paying premiums for 3 years, you shall be eligible to receive a Surrender Benefit.

Your Surrender Benefit will consist of your guaranteed surrender value and any non-guaranteed surrender value, such as a declared performance bonus.

However do take note that by surrendering your plan early, you shall be subjected to high fee amounts which greatly lowers your surrender value. Such high charges may result in your eventual surrender value is even lesser than the amount of premiums you have paid.

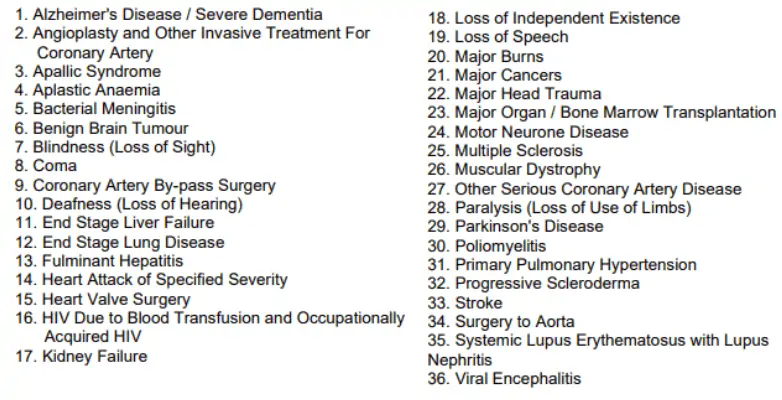

Coverage Add-ons (Riders)

| Additional Riders (Optional) | Description |

| Accident Assist |

|

| Early Stage Crisis Waiver |

|

| Crisis Waiver III |

|

| Early Payer Security |

|

| Payer Security III / Payer Security Plus | Helps to look after your loved one’s policy in the case where death, critical illness, or total and permanent disability happens to you. |

| |

| Crisis Cover III |

The following list shows the critical illness coverage under this rider:

Benefit Amount

|

Fees and charges

You will be happy to note that there are essentially no fees and charges for the policy as the minimum premium amounts mentioned above are net, meaning that the fees and charges have already been taken into consideration.

How much will I receive upon maturity of the PRUFlexi Cash?

The table above assumes the following:

- The return rate of investment is 4.75% per annum.

- Person Assured is a 25-year-old male who does not smoke.

- The assured sum of S$120,000.

- Yearly Cash Benefit chosen to be paid out from the 2nd policy year-end.

In the scenario where you don’t make any withdrawals and accumulate the full amount, pay S$12,568 yearly, and choose the 15-year term, you will receive a total potential payout sum of S$211,433 at age 40. As seen in the table above, you will be receiving a guaranteed Yearly Cash Benefit of S$6,000 starting from the end of your 2nd policy year.

Below are the calculations:

Total Premiums Paid:

S$12,568 x 15 years = S$188,520

| Guaranteed Portion | Non-Guaranteed Portion | |

| Policy Year 2-14 | S$6,000 x 13 years = S$78,000 | – |

| Policy Year 15 (Maturity Benefits) | 55% x S$120,000 = S$66,000 Since the insured selected the 15-Year term and Yearly Cash Benefits from the end of his 2nd policy year, his maturity benefit is 55% of his sum assured as stated in the table from the Maturity Benefit Section | S$67,433 |

| Total | S$144,000 | S$67,433 |

| Grand Total: | S$211,433 | |