Tokio Marine’s GoTreasures is an investment-linked plan (ILP) that allows you to customise your plans according to your needs and wants, giving this product an edge over others due to its flexibility.

It also gives you 5 different currencies to invest in, adding to the flexibility it offers.

However, how good is it and how well does it stack up to other ILPs in the market?

Here’s our review of it, continue reading to find out.

My Review of the Tokio Marine GoTreasures

If you don’t already know, GoTreasures is an alternative to Tokio Marine’s GoClassic. Both ILPs offer similar flexibility, bonuses, and the same funds.

The main difference between them is that GoClassic’s minimum investment amount is S$630, while GoTreasures’ is $300 monthly. The policy charge on GoTreasures is also higher at 1.5% as compared to GoClassic’s 1.35%.

The reduction in minimum investment amount is substituted with higher fees in Tokio Marine’s GoTreasures.

Based on my calculations, the GoClassic performs better at 458.76% under similar conditions as the GoTreasures. However, as I do not have the breakeven table for Tokio Marine’s GoTreasures, it is likely that GoTreasures will perform better once bonuses are included.

However, compared to other ILPs in the market, the death benefit only covers 101% of your policy value instead of the higher of 101% of your policy value or net premiums.

This means that if you were to pass on during a market correction or crash, there’s a possibility of receiving less than the premiums you’ve paid.

All in all, if you are looking for a flexible investment-linked plan which has the potential to offer you returns for the long-run, GoTreasures will be a good product to consider.

Not only do you have a range of well-performing funds to choose from, you also have a choice of adjusting and topping up or paying for additional premiums, whenever you decide to.

It’s also been categorised as one of the best investment plans in Singapore in our 2021/2022 edition of our post.

However, with new product entrants and revisions made to other ILPs in the market, the Tokio Marine #goTreasures is no longer in our list.

For instance, the Manulife InvestReady III is the overall best ILP, best for dividend payouts, and best for those looking for a flexible ILP.

A close competitor to them would be the Singlife Savvy Invest, which has the highest potential to generate the most returns for you.

Not forgetting FWD’s Invest First Plus, which has the lowest fees in the market and pretty good selection of funds to choose from – with its downside being the long investment periods you’ll have to commit to.

Because of the many options to choose from, the long and heavy commitment needed from investment plans (20 to 30 years of a few hundred dollars per month), you should really take some time to understand what are your available alternatives.

We suggest reading our comparison on the best ILPs to get yourself started.

Once you understand your options, you should consider getting a second opinion from an unbiased financial advisor to see if the Tokio Marine #goTreasures is truly the best choice for you.

If you need someone to get a second opinion from, we partner with MAS-licensed financial advisors who are more than happy to assist you.

Click here for a non-obligatory chat.

Now let’s dive into what the Tokio Marine #goTreasures offer.

Overview: Key Features of the Plan

Choosing from 5 different currencies

With this plan, policyholders can choose their preferred choice of currency – whether it is SGD, AUD, GBP, EUR, or USD.

Choose your commitment term

After you have selected the currency you are comfortable with, you can also choose your premium payment terms from anywhere between 10 to 30 years.

With these premiums paid, 100% of your money will be directed by Tokio Marine into funding your investment.

Customising Your Plan as You Grow

As you grow into different seasons and stages, GoTreasures also allows you to top up your plan with single recurring premiums or top-up premiums, if you have the financial capacity to do so.

Furthermore, there is also an open option to switch funds.

No Charges for Partial Withdrawals and Premium Holidays

Should you need to liquidity some of your funds and withdraw additional monies at any point in your premium payment term, Tokio Marine GoTreasures does not impose any charges.

From your 3rd year onwards, you can also take unlimited premium holidays, as and when you need them.

Now that you have gotten a quick overview of what this plan offers, we will go into further detail about the nitty-gritties of what sets this ILP apart from others.

General Features

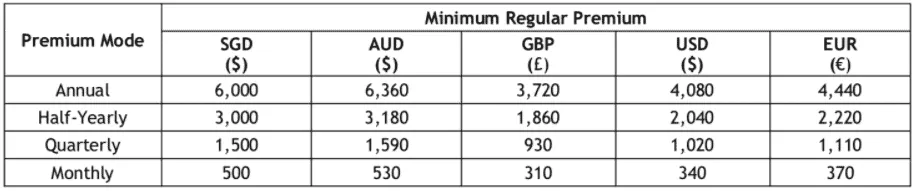

Regular Premium Payment Terms

With 5 major currencies and a variety of payment premium modes, policyholders can choose how often they wish to pay for their premiums.

Since you have the option of committing between 10 to 30 years, this table below shows the regular premiums you will be paying if your payment term spans from 10 to 19 years:

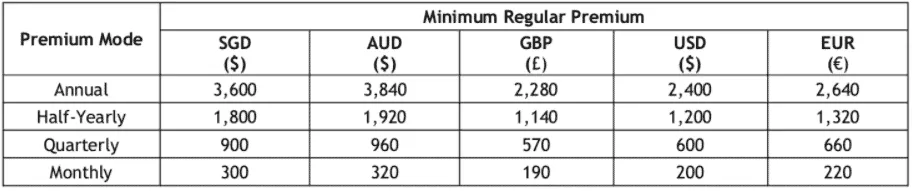

Alternatively, if you are opting for a premium payment term of 20 to 30 years, your premiums will be as follow:

Premium Allocation

All the regular premiums paid will be channelled into purchasing units, which will be allocated to your Initial Units Account during the first 2 years.

From the 3rd year onwards, any units purchased using your regular premiums will be allocated to your Accumulation Units Account.

Initial Units Account VS Accumulation Units Account

Before we get confused about these jargons, let us go through a brief summary of what the Initial Units Account (IUA) and Accumulation Units Account (AUA) are for. Simply put, these are accounts where your allocated units will be found.

| Account Type / Fund Units Purchased | Basic fund units purchased with regular premiums will be allocated here if: | Other types of funds will be allocated here: |

| Initial Units Account (IUA) | Purchased during first 24 months | Units purchased with Initial Bonus |

| Accumulation Units Account | Purchased anytime after 24th month | Any recurring single premiums, top-up premiums, units purchased with Loyalty Bonus |

Plan Flexibility

Redeeming your Units

Tokio Marine GoTreasures offers the flexibility of withdrawal from your Initial Units Account and Accumulation Units Account, even during your premium payment term.

Yet, this is on one condition – that even after you have redeemed your units, your accounts still fulfil the minimum account value, which will be decided by Tokio Marine.

Partial Withdrawals

From the 3rd year onwards of your plan, you are entitled to withdraw partial amounts from your policy. However, this has to be done with a minimum of $500 with each transaction.

There are 2 different ways you can receive your withdrawal:

- From only your Accumulation Units Account, if you are withdrawing during the premium payment term

- From the Initial Units Account and Accumulation Units Account, if you are withdrawing after the premium payment term

For the case of a partial withdrawal from your AUA, typically the minimum account value will be set at $3,000 but this value can also vary from time to time, as Tokio Marine deems fit.

Regular Withdrawal

Apart from a one-off withdrawal, GoTreasures also allows for policyholders to withdraw regularly from either the Initial Units Account and/or the Accumulation Units Account.

Depending on your preference, you can exercise this withdrawal during or after your premium payment term. You can do so either annually, half-yearly, quarterly, or monthly – all you need is a written request.

Reduction in Regular Premiums

What if I am unable to continue paying for the same amount of premiums as I have been paying for?

Fret not – with the flexibility of GoTreasures, you will be able to reduce your regular premiums in the 3rd year onwards of your plan. This is, however, in the case that you have completely paid for your regular premiums in the first 2 years.

Still, do note that there is a minimum reduction amount, as well as a minimum regular premium you would still have to commit to. So while you do have the flexibility to reduce your regular premiums, there are still certain requirements to be fulfilled.

The minimum reduction amount will differ over time, as determined by Tokio Marine

Increase in Regular Premiums

If you have previously reduced your regular premiums, you now have the option to increase it back, should you decide you have the financial capacity to again.

Similar to reductions, there are also minimum increments in the regular premium amounts you have to pay. The minimum increment amount will also differ over time, as determined by Tokio Marine.

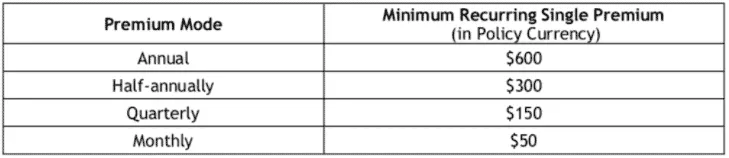

Recurring Single Premiums

Recurring single premiums are smaller sums of money that you can repeatedly put into your account on a stipulated interval basis, with 100% of these premiums being used to purchase units that will be allocated to the Accumulation Units Account (AUA).

Even while you are on a premium holiday, you can still continue paying for the recurring single premium. However, this is with the condition that your regular premium payments have already resumed at the annual rate which has been agreed upon during the commencement date.

Here, you can have a look at the minimum single premium required for each mode:

Similar to regular premiums, you can choose to increase or decrease these recurring premiums, or completely stop paying for them. All it takes is a letter in writing to inform Tokio Marine of your decision.

There’s no rush to make this decision as your recurring single premiums can be made either on the day of your policy purchase, or even after the commencement date.

Premium Top-ups

If you’re considering topping up a larger lump sum at any point during your policy, you can also do so – provided you are investing a minimal amount of $3,000.

All the top-up premiums paid will be channelled into purchasing units which will be allocated into your Accumulation Units Account.

Premium Holiday

Re-visiting one of the highlights of GoTreasures, this plan offers policyholders the option of stopping payment for their regular premiums after the first 2 years.

Your basic plan will not be terminated, as long as you have adequate value in your policy for deduction of termly fees.

How Riders are Affected on a Premium Holiday

If you had previously opted for a rider, your rider will be converted into a unit-deducting rider. Simply put, this means that your coverage will only include the event of a death or injury which was caused solely and directly by accidents.

The premiums required for this rider will be paid monthly through the Accumulation Units Account. However, if there is an insufficient amount in your account, your rider will instead be automatically cancelled when the premium holiday starts.

Adding, Removing and Changing Life

The flexibility of GoTreasures allows policyholders to add, remove, or change the lives assured with ease at any juncture of the plan.

However, there are certain criteria you have to meet before deciding to add a new life to the policy:

- The sum of his age and the remaining premium payment terms do not exceed 75 years. Typically, this will not be an issue unless the new life assured is elderly.

- The new life assured is 1 month old. This means that parents who are intending to insure their newborns can do so too.

- If the policyholder had purchased the Advanced Death Benefit prior, its monthly protected charge will be now adjusted based on the age and gender of the oldest life assured in the policy

- There is proof of insurable interest in the new life assured during the application process

Full Surrender

In the case where you decide you want to request for full surrender, there are 2 possible scenarios in which you will receive your surrender value:

- While the policy is still in force during the premium payment term – the surrender value less indebtedness shall be paid out, if there are any.

- After the premium payment term – the policy value less indebtedness will be paid out.

The indebtedness amount refers to any amount that is owed to Tokio Marine. Only after these are being paid, will your policy officially terminate.

Termination of Policy

Apart from the breach of terms and conditions, other causes such as the following will also lead to the automatic termination of policy:

- When the last life assured has passed away

- Full surrender by the policyholder

- The policy value is inadequate and cannot pay for any charges

- The policy value is lower than the Minimum Account Value

- Non-fulfilment of regular premium payment during the first 2 years of the policy

Protection

As per your death benefits, you are only entitled to select them at the start of your policy. After the commencement of the plan, you are not allowed to change it.

Basic Death Benefit

In this case, they will receive 101% of the policy value less indebtedness.

Advanced Death Benefit

If the death happened during premium payment term:

The beneficiary will either receive 101% of policy value less indebtedness or 100% of Net Premium – whichever is higher.

This net premium refers to all the types of premiums that the policyholder might have had paid for prior to his death, excluding the amounts which have been withdrawn.

If the death happened after the premium payment term:

The beneficiary will receive 101% of policy value less indebtedness.

Key Features

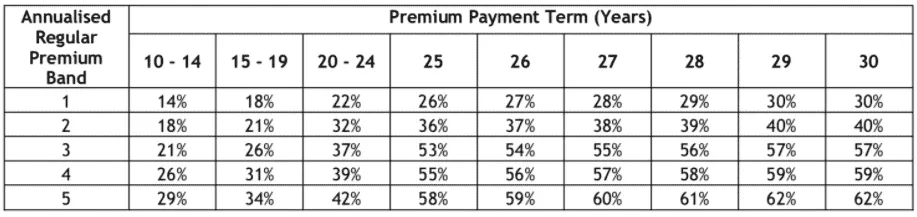

Welcome Bonus

Once you have signed up for the policy successfully, you will receive an initial bonus within the first 3 years, allocated to your Initial Units Account.

This bonus you receive will be in accordance with your regular premium band. For a gauge, your plan will fall under band 1 if your annual premiums are less than SGD $12,000 and a maximum of band 5 if you are paying more than SGD $48,000.

Loyalty Bonus

To reward you for committing to GoTreasures, Tokio Marine will also offer loyalty bonuses from the fourth year onwards, with the following rates:

Not only will you receive a loyalty bonus during your premium payment term, you will also receive it even after the end of the premium payment term – as long as your policy is still in force. Your loyalty bonus will be allocated to your Accumulation Units Account.

Receive Dividend Payouts

When receiving your dividends from these funds, you can either opt to:

- Receive it in cash

- Re-invest – in which Tokio Marine will pay these dividends to you if it’s $50 and above. Otherwise, they will be re-invested, again, as additional units in your sub-fund of choice.

Either way, your dividends will be paid out to you within 30 days of the end of its declaration date.

Fund Offerings

Types of Funds

Tokio Marine GoTreasures primarily invests in mutual funds. These are funds that are managed by another team or firm apart from where the units are being held – in this case, by PricewaterhouseCoopers LLP (PwC).

While you might not be well-acquainted with this name, what you might be assured to know is that PwC’s clients include some of the biggest companies such as Bank of America, IBM, Goldman Sachs, and the like.

This plan offers three main fund categories:

- Fixed-income funds:

Mutual funds which mainly invest in bonds and other debt securities (e.g. government bonds, corporate bonds, high-yield bonds, etc.).

These funds are best for generating income or preserving your capital.

- Multi-asset funds:

As the name suggests, this fund includes more than one asset class to create a combined portfolio of cash, equity and/or bonds.

The upside of this provides investors with greater exposure and range.

- Equity funds:

Essentially, this helps policyholders increase their capital through stock investment, mostly done in equity securities in listed shares.

These funds are recommended for those who are set out for long-term capital growth.

Fund Switch

In the event that you wish to switch any units from one fund to the other, you will have to transfer a minimum amount during each fund switch. Additionally, the value of units in both your original and target fund should also fulfil the minimum amount required after the switch.

However, do note that you are not able to switch your units from Initial Units Account to Accumulation Units Account, and vice versa.

Tokio Marine GoTreasures Top 10 Performing Sub-Funds

| Name of Fund | 5-Year Historical Average (%) |

| Franklin Technology Fund Acc USD (TABU) | 32.21 |

| FSSA Greater China Growth Fund Acc USD (AABU) | 20.03 |

| Schroder ISF China Opp Acc USD (SAAU) | 19.72 |

| FSSA Regional China Fund Acc SGD (AABS) | 19.72 |

| Schroder ISF China Opp Acc SGD-H (SAAS) | 18.76 |

| Fundsmith Equity Fund Acc GBP (1AAG) | 17.65 |

| Fidelity European Dynamic Gr Acc USD-H (FACU) | 15.72 |

| Fidelity European Dynamic Gr Acc SGD-H (FACS) | 15.00 |

| Fidelity Asian Special Sit Dis USD (FAAU) | 14.51 |

| Fidelity Emerging Markets Acc USD (FABU) | 14.47 |

Accurate as of June 2021.

Past performance does not dictate future returns.

Fees Involved

| Type of Charge | Rate | Who does it involve |

| Initial | 5.4% p.a. on IUA | All Policyholders |

| Policy | 1.5% p.a. on IUA and AUA | All Policyholders |

| Premium: Recurring Single Premium and Top-up Premium | 5% on each premium

Charge will be deducted prior to allocation of premium to the policy |

Those who make premium top-ups on top of their basic premiums |

| Monthly Protection | Levied during the first 2 years of policy via AUA; paid in a lump sum for the third year

Should there be insufficient amounts in your AUA, Tokio Marine will automatically change the death benefit to a basic death benefit coverage, and you will not be allowed to revert these changes. MPC applies even while on premium holiday. |

Policyholders who opted for Advanced Death Benefit |

| Third-Party | All bank charges associated with receipt of premiums proceeds to the policyholder | |

| Surrender | To multiply IUA value by applicable rate during year of surrender | Policyholders who end their premium payment term prematurely |

| Credit Card | 1.6% | Policyholders who paid premiums via credit cards |

| Fund Management Fee | Already accounted for in unit price, no additional charge | All policyholders |

| Policy Currency Change | NIL | |

| Switching | NIL | |

| Administrative | NIL | |

| Partial Withdrawal and Regular Withdrawal | NIL | |

Compulsory Fees

There are some fees that won’t apply to you. These are the mandatory fees you’d incur if you committed to a policy (in SGD) from its inception to its maturity:

- Initial Charge (5.4% p.a. of the initial units account)

- Policy Charge (1.5% p.a. of the policy value)

Based on this, the compulsory fees you incur on the Tokio Marine GoTreasures is 6.9%. However, it’s only for the first 2 years. Furthermore, this is overestimated as the initial charge is based only on your initial units account while your policy charge is 1.5% of the policy value.

How much will I receive upon maturity of the Tokio Marine GoTreasures?

The calculation was done for you by a Tokio Marine representative.

Suppose you invest $300 monthly for 20 years and let it compound for another 10 years, the funds have a 10-percent annual return, you have made no withdrawals, and you haven’t taken any premium holidays; you can expect:

|

First 2 Years |

|

| Monthly premium: | $300 |

| Premium Payment Term: | 20 years (240 months) |

| Annual Fund Performance: | 10% |

| Fees in the first 2 years: | 6.9% |

| Net Fund Performance for the first 2 years: | 3.1% |

| Investment value: | $7,630.49 |

|

Next 10 Years |

|

| Fees in the next 10 years: | 1.5% |

| Net Fund Performance in the next 10 years: | 8.5% |

| Total Investment Value: | $174,697.84 |

|

Next 10 years |

|

| Fees in the last 10 years: | 1.5% |

| Net Fund Performance in the last 10 years: | 8.5% |

| Total Investment Value: | $394,988.92 |

Total Premiums paid after 20 years: $72,000

Total Interest Earned: $322,988.92

ROI: 448.60%

References

https://www.comparefirst.sg/wap/prodSummaryPdf/194800055D/ULE_UNXD_TPDN_CIN_Summary.pdf

https://www.tokiomarine.com/sg/en/personal/wealth/wealth-planning/goTreasures.html